Global semiconductor equipment sales will hit a record high in the next three years

Published: 9.30.2024

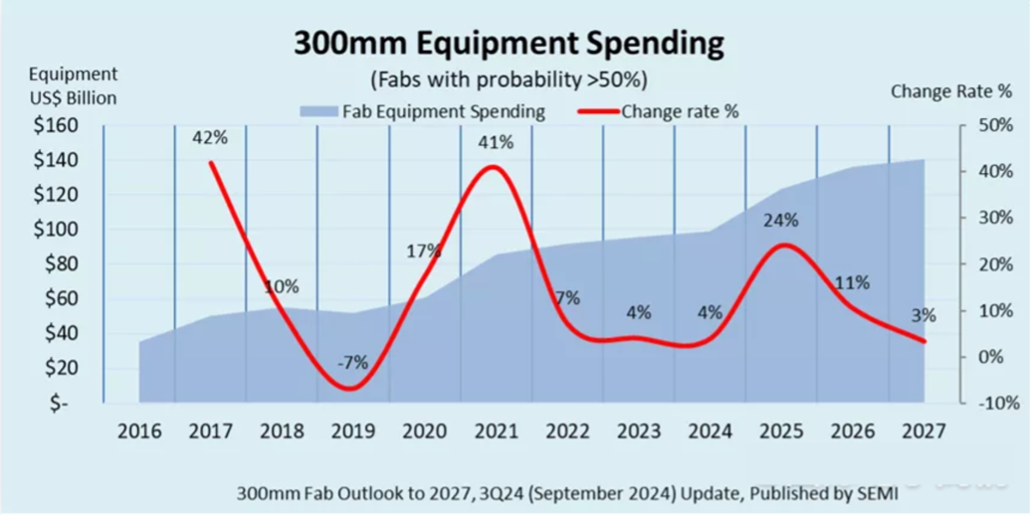

The Semiconductor Industry Association (SEMI) predicts in its 300mm Fab Outlook Report to 2027 that semiconductor manufacturers are expected to spend a record $400 billion on semiconductor equipment in the three years between 2025 and 2027, driven by growing demand for artificial intelligence (AI) chips used in data centers and edge devices, with China, South Korea, and Taiwan area spending the most.

In terms of specific regional performance, SEMI said that driven by China's national policy of self-sufficiency, China's semiconductor manufacturers will spend more than $100 billion on semiconductor equipment in the next three years, and will continue to be the world's largest semiconductor equipment market. However, the report also added that Chinese semiconductor manufacturers' equipment spending will decline from a record $45 billion this year to $31 billion in 2027.

South Korea is expected to spend $81 billion on semiconductor equipment in the next three years, thanks to the help of memory chip manufacturers Samsung and SK Hynix.

Thanks to the continued investment of foundry giants such as TSMC, Taiwan area will push its capital expenditure in the semiconductor equipment field to US$75 billion in the next three years. It should be noted that TSMC currently also has factories in the United States, Japan and Europe.

In the Americas, it is expected to invest US$63 billion in the semiconductor equipment field in the next three years, while Japan, Europe, the Middle East and Southeast Asia are expected to invest US$32 billion, US$27 billion and US$13 billion respectively in three years.

SEMI also forecasts growth in the market segments in the report. Wafer foundry equipment spending is expected to reach approximately $230 billion between 2025 and 2027, driven by investments in cutting-edge nodes below 3nm and continued spending on mature nodes. Investments in 2nm logic processes and the development of 2nm key technologies, such as gate-all-around (GAA) transistor structures and backside power supply technology, are critical to meeting future high-performance and energy-efficient computing needs, especially for artificial intelligence applications. Cost-effective 22nm and 28nm processes are expected to grow due to growing demand for automotive electronics and IoT applications.

The logic and microelectronics sector is expected to lead equipment spending expansion over the next three years, with total investments expected to reach $173 billion. The memory sector ranks second and is expected to contribute more than $120 billion in spending during the same period, marking the beginning of another market segment growth cycle. In the memory sector, investments in DRAM-related equipment are expected to exceed $75 billion, while investments in 3D NAND are expected to reach $45 billion.

Power-related fields ranked third, with an expected investment of more than $30 billion over the next three years, including about $14 billion in compound semiconductor projects. The analog and mixed-signal field is expected to reach $23 billion in the same period, followed by the optoelectronics/sensor field with an investment of $12.8 billion.